Week 21 / $98 Premiums, NVDA Volatility, and DOCU Position

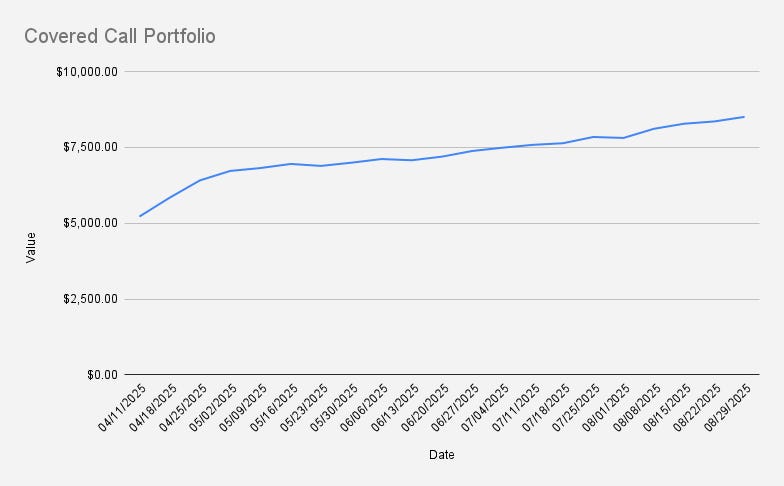

As of August 29, 2025, our covered call stock portfolio stood at $8,504, what is another weekly increase of +1.81% (+$150). While Year-to-date, our portfolio is +8.87%. Awesome!

This week, we collected $98 from selling options, what is slightly above my goal to generate at least 1% weekly in options premium (1.15% this week).

Our portfolio remains concent…