Smoking Out Profits: Dividend + Covered Calls and the Unexpected Strength of BTI

British American Tobacco (BTI) has long been a polarizing name in the investment world. As one of the largest tobacco companies globally, it operates in an industry often labeled as "dying" due to declining cigarette consumption and increasing regulatory pressures.

Yet, to my surprise—and perhaps to the surprise of many—BTI and its tobacco peers have shown remarkable resilience in recent years. As an investor who has been actively trading BTI since the summer of 2023, I’ve experienced the stock’s volatility firsthand, leveraging put options (specifically credit spreads) and, more recently, considering the merits of covered calls.

What started as a challenging journey with underwater positions has ultimately turned into a positive experience, culminating in a modest profit as I shift my focus toward building my NVIDIA (NVDA) portfolio.

My BTI Journey: From Credit Spreads to a Single Share

My foray into BTI began in the summer of 2023, driven by its attractive valuation and high dividend yield—currently hovering around 7-8%, depending on the stock price.

At the time, I saw an opportunity to generate income through options, specifically by selling put credit spreads.

Initially, things didn’t go as planned. BTI’s stock price faced downward pressure, and my credit spreads quickly went underwater. For a while, I found myself rolling out suffering positions—extending the expiration dates and adjusting strike prices to avoid losses and buy time for a recovery. It was a grind, and I’ll admit there were moments when I questioned my decision to dive into tobacco stocks. The market seemed to agree with the narrative that tobacco was a fading industry, and BTI’s stock price reflected that sentiment, trading at a low multiple of its earnings and free cash flow.

But patience paid off. Over time, BTI began to stabilize and even rally, buoyed by strong earnings reports and growing momentum in its "new categories" business—vaping, heated tobacco, and oral nicotine products like pouches.

By late 2024, my options trades had recovered, and I eventually closed most of my positions, leaving me with just one share of BTI. Holding that single share felt symbolic of my journey—a small remnant of a strategy that had tested my resolve. Recently, with the stock trading profitably, I decided to sell it, locking in a gain and redirecting my capital toward NVDA shares, where I see greater long-term growth potential.

Tobacco’s Surprising Resilience

Despite my initial skepticism about tobacco as a "dying industry," the performance of BTI and other tobacco stocks has been eye-opening. While global cigarette volumes are indeed declining, companies like British American Tobacco have adapted by leveraging pricing power in traditional cigarettes and diversifying into next-generation nicotine products.

BTI’s Vuse vaping brand, for instance, has gained significant traction, and its oral nicotine pouches are growing at an impressive clip—some reports suggest 50% year-over-year growth in that segment. Meanwhile, the company’s combustible cigarette business, which still accounts for over 80% of revenue, continues to generate robust cash flows, supporting a generous dividend.

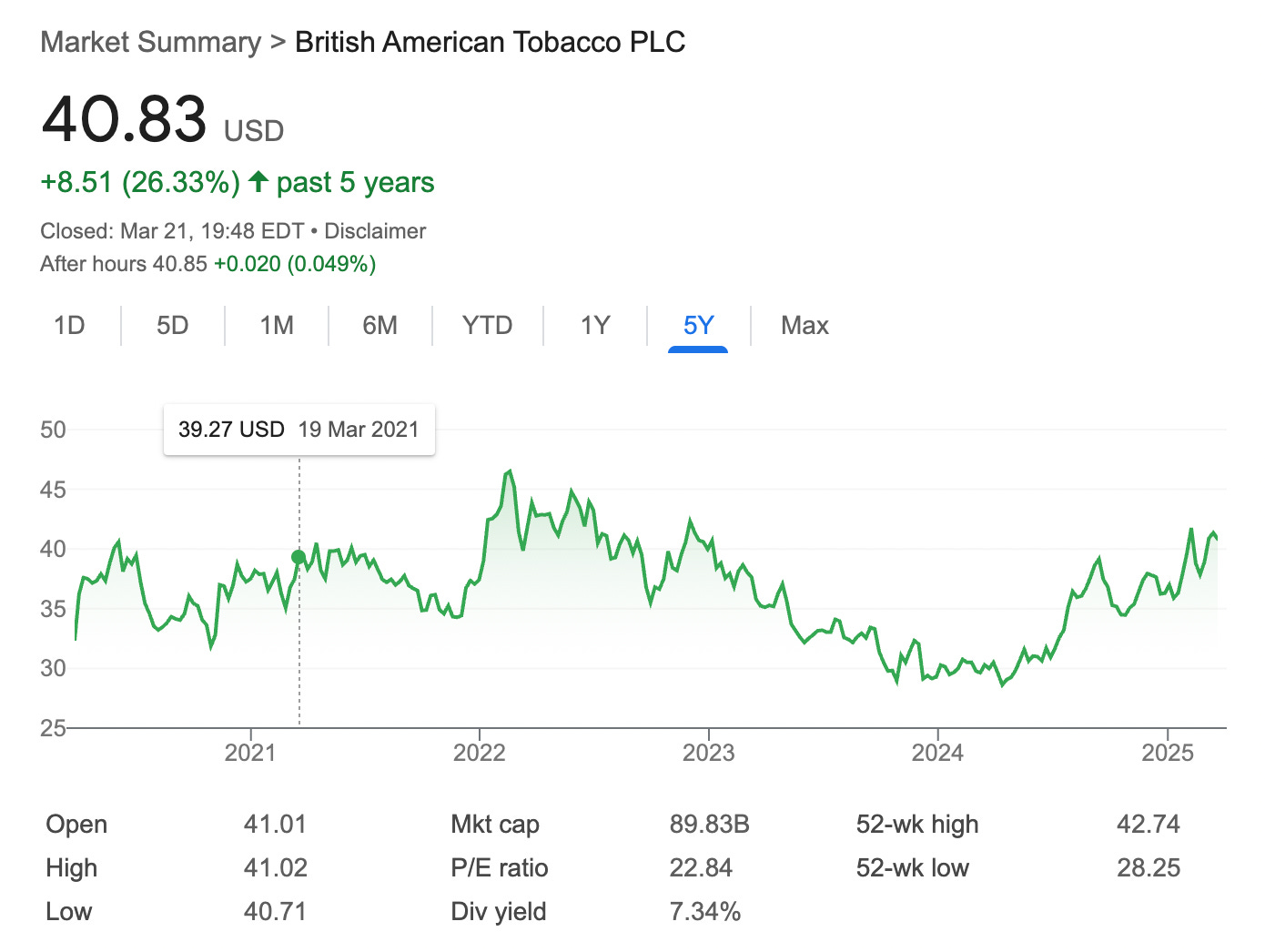

This resilience is reflected in BTI’s stock performance. As of March 23, 2025, the stock has delivered solid total returns when factoring in its dividend, even if share price appreciation alone has lagged broader market indices like the S&P 500.

Analysts point to BTI’s valuation as a key draw: trading at roughly 8-9 times forward earnings and 7-8 times free cash flow, it’s a bargain compared to peers like Philip Morris International (PM), which trades at 21-22 times earnings. For income-focused investors, this combination of a low valuation and a high, sustainable dividend yield (with a payout ratio around 60%) makes BTI a compelling option.

Analyst Recommendations on BTI

Stock analysts have mixed but generally positive views on BTI as of early 2025. According to data from sources like TipRanks and MarketBeat, the consensus rating leans toward a "Moderate Buy" or "Hold," depending on the sample size. For instance:

Barclays recently raised its price target to 3,550 GBp (approximately $45 USD at current exchange rates) from 3,450 GBp, maintaining a "Buy" rating, citing BTI’s improving margins and smokeless product growth.

UBS also holds a "Buy" rating, with a target suggesting upside from current levels, pointing to the company’s undervaluation and cash flow strength.

Morgan Stanley, however, is more cautious, assigning a "Sell" rating with a lower target of 2,650 GBp, highlighting regulatory risks and a slower-than-expected transition away from combustibles.

Seeking Alpha contributors have noted BTI’s 8.5-9% free cash flow yield and 7+% dividend yield as reasons to consider it a "blue-chip bargain," though some downgraded it to "Hold" due to lingering combustible reliance.

The average 12-month price target from analysts hovers around $34.50-$38, implying modest upside or downside depending on the current price (recently around $38-$39). This range reflects the tug-of-war between BTI’s value proposition and the secular challenges facing tobacco.

Covered Calls: A Natural Fit for BTI?

Given my experience with options, I’ve often considered whether selling covered calls on BTI would have been a better fit during my holding period.

BTI strikes me as an ideal candidate for covered calls, and here’s why I think it’s worth exploring:

High Dividend Yield + Option Premiums: With a 7-8% annual dividend, BTI already offers a strong income stream. Selling covered calls could boost that yield further, potentially pushing annualized returns into the double digits if timed well. For example, selling a near-term, slightly out-of-the-money call might yield 1-2% in premium per month, adding 12-24% annualized income on top of the dividend.

Low Volatility: Despite occasional dips, BTI’s stock price tends to be less volatile than growth stocks like NVDA. This stability makes it easier to sell calls at strike prices you’re comfortable with, reducing the risk of the stock surging past your strike and being called away unexpectedly.

Sideways Price Action: BTI has historically traded in a range rather than posting dramatic gains. For covered call sellers, this is perfect—you can repeatedly sell calls, collect premiums, and retain the shares as long as the stock doesn’t break out significantly.

In my case, I only held one share by the end, so covered calls weren’t an option (you need 100 shares per contract). But if I were to rebuild a BTI position, I’d seriously consider this strategy. For instance, with the stock at $39, selling a $40 call expiring in a month might net $0.50-$1 in premium, offering a 1.3-2.5% return in just 30 days—plus the dividend if held through the ex-date.

Why I’m Moving On (For Now)

While my BTI experience has been positive overall, I’ve decided to sell my last share and pivot toward NVDA. This shift isn’t a reflection of lost faith in BTI but rather a strategic choice to consolidate smaller holdings and focus on growth opportunities. NVDA, with its dominance in AI and semiconductors, offers a higher ceiling for capital appreciation, even if it lacks BTI’s income appeal.

After years of managing options trades and watching tobacco defy expectations, I’m ready to simplify my portfolio and bet on a different sector.

That said, I wouldn’t rule out returning to BTI—or even tobacco stocks broadly—in the future. The industry’s ability to adapt, combined with BTI’s cash flow machine and dividend reliability, keeps it on my radar. For now, though, I’m content to take my profit and move on.

Final Thoughts: Should You Sell Covered Calls on BTI?

If you’re an income-focused investor with a stomach for tobacco’s ethical and regulatory baggage, BTI is worth a look—and covered calls could amplify its appeal. The stock’s undervaluation, steady cash flows, and high yield make it a strong foundation for this strategy. The premiums, paired with the dividend, could turn BTI into a reliable income generator, even in a "dying" industry that keeps proving it’s got life left.

For me, BTI was a lesson in resilience—both the stock’s and my own. And while I’m stepping away for now, I’ll be watching from the sidelines, curious to see how this tobacco giant continues to defy the odds.