NVDA Surge, NFLX Credit Spreads and a Record $245 Options Income Week

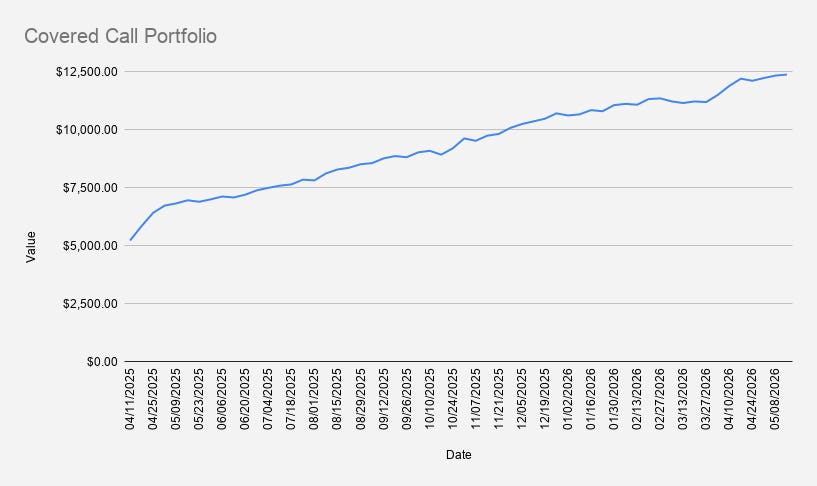

As of May 15th, 2026, our stock portfolio powered by options trading increased by another +0.36%, reaching $12,367.

On a year-to-date basis, the portfolio is now up 18.95%, outperforming the S&P 500 (+8.18%), though still slightly trailing NVDA itself, which gained +20.38% over the same period.

This week was largely driven by a massive rally in NVDA stock…