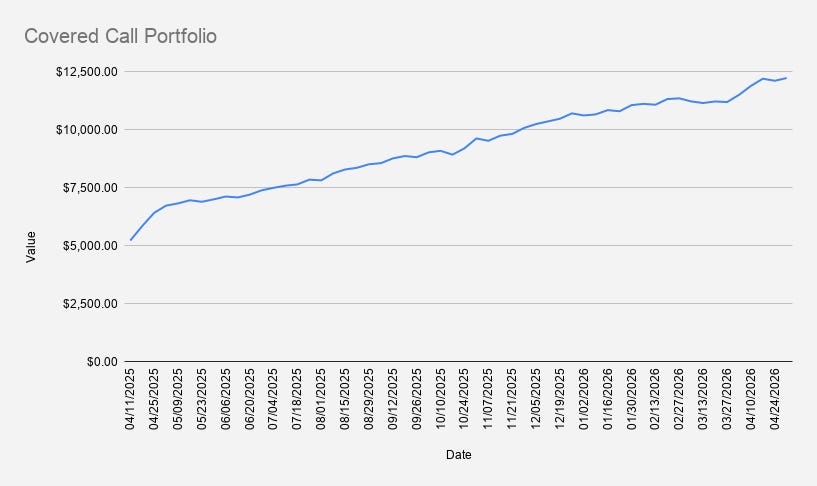

How NVDA Pullback Boosted Our Options Income Strategy (+0.97%)

As of May 1st 2026, our options trading driven stock portfolio increased slightly by +0.97%, closing at $12,218.

This week was one of the rare times I didn’t mind seeing NVDA drop—from $210 to below $200. As a put seller, sharp rallies are actually uncomfortable: premiums compress, entries get worse, and the risk of a sudden pullback increases. That’s ex…