Credit Spread Trade Management: Rolling an NFLX Position Into a Cash-Secured Put

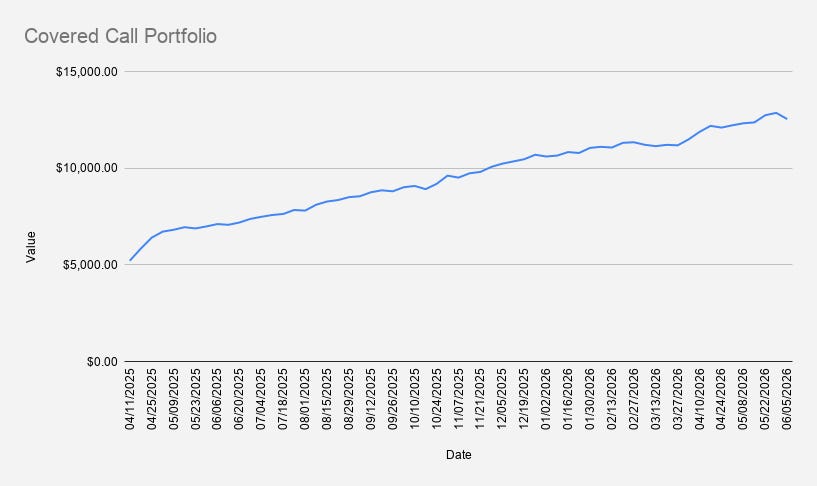

Portfolio Value: $12,540

Weekly Change: -2.5%

YTD Return: +21.07%

Options Premium Collected: $157

On June 6, 2026, the portfolio value declined by -2.5% compared to the previous week, reaching $12,540.

The decline was not entirely driven by stock performance. Currency movement played a role as well. The U.S. dollar strengthened against the euro, with EUR/USD…